Traditional financial technology has enabled the modern global commerce and industry to flourish, but its limitations are becoming increasingly apparent as decentralized finance (DeFi) matures.

Global commerce banks, central banks, global acquirers like BCW partner Worldpay, and credit card companies facilitate payments and cross-border money transfers via traditional systems that are now rapidly evolving to accommodate more growth.

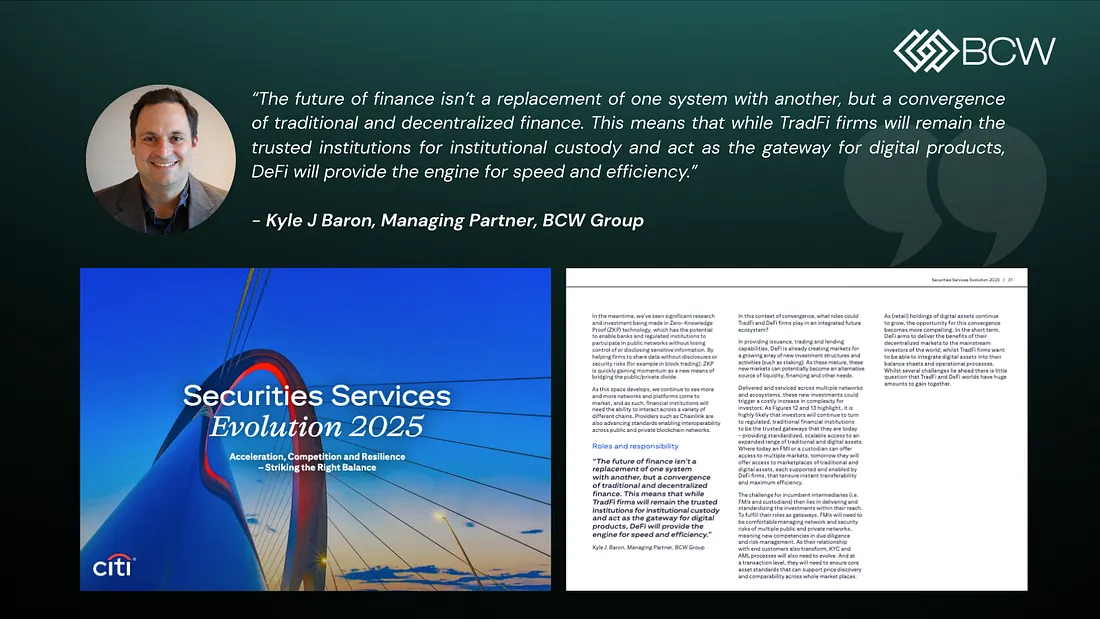

The eventual marriage of traditional finance (TradFi) and DeFi could usher in a new phase of expansion that enables more people to gain access to financial services than ever before.

To learn more about how TradFi institutions are adopting DeFi technology, visit our blog and check out stakefi.network, the institutional standard for digital asset yield.

What is Traditional Finance?

At its core, TradFi is a permissioned system built on institutional trust. The primary stakeholders act as the gatekeepers and sources of truth for every transaction as they vouchsafe the ledgers used to record account balances.

Technologically, TradFi operates on a fragmented back end of private, siloed databases with COBOL at its core.

Much of the world’s banking, and over 40% of US banking systems rely on COBOL mainframes, which necessitates a process called reconciliation. Because your bank’s ledger cannot see another bank’s ledger in real-time, they manually sync their books at the end of each day.

SWIFT and Payments

There is also SWIFT, the primary messaging rail for over 11,500 institutions, sending the encrypted instructions required to trigger cross-border payments without actually moving the physical funds themselves.

As of 2026, SWIFT has fully transitioned to the ISO 20022 standard, moving the industry away from legacy messages toward a data-rich XML format designed to reduce manual reconciliation and technical debt.

When you make a payment, money doesn’t move instantly; instead, a series of digital handshakes occurs. While it may seem a mundane task at the point of sale, a single swipe involves a complex chain of events. An issuing bank authorizes the funds, a payment processor routes the data through SWIFT, and a clearinghouse settles the debt days later.

This reliance on manual batching and multi-layered intermediaries is why a standard domestic transfer can take 48 hours to clear. Each of these interactions on the back end incur fees, which compounds the time and cost of payments at scale.

The Difference With DeFi

DeFi is an open-source financial ecosystem built on public and private blockchains that removes the need for traditional intermediaries.

Unlike TradFi’s closed and trusted model, DeFi is a modular ecosystem of decentralized apps (dApps) where trust is established through auditable code.

See how BCW is active in the DeFi space with interoperability solutions, institutional staking, and enterprise-grade infrastructure.

The human element of DeFi comes from Decentalized Autonomous Organizations (DAOs) that govern protocol rules. DAOs are run by individual governance token holders who have the power to vote on DeFi platform operations.

Open market effects also impact DeFi platform operations as any user can become a liquidity provider. Because they self-custody their funds as onchain cryptocurrency, they can move liquidity between pools at will depending on where incentives are highest. As a result, exchange rates on currency swaps, such as between stablecoins like Circle’s USDC and Tether’s USDT, can be in a constant state of flux.

Payments in DeFi flow through atomic settlement, wherein the transfer of value and the update of the ledger happen simultaneously. When a user initiates a transaction, it is queued by the blockchain protocol, verified by a global network of decentralized nodes, and finalized in minutes, and sometimes seconds. This process tends to be cheaper for the end-user.

The DeFi Tech Stack

Technologically, DeFi replaces private bank ledgers with a transparent settlement layer on a blockchain. Manual reconciliation is replaced by smart contracts.

Smart contracts are self-executing code that automatically trigger transactions when specific conditions are met.

DeFi is maturing into an institutional-grade tech stack for privacy and compliance that includes AI-driven risk engines and Zero-Knowledge Proofs. BCW Technologies and Arkhia are at the forefront of the ZK technology frontier by offering enterprise-grade Web3 privacy solutions with ZK Provers-as-a-Service.

TradFi & DeFi

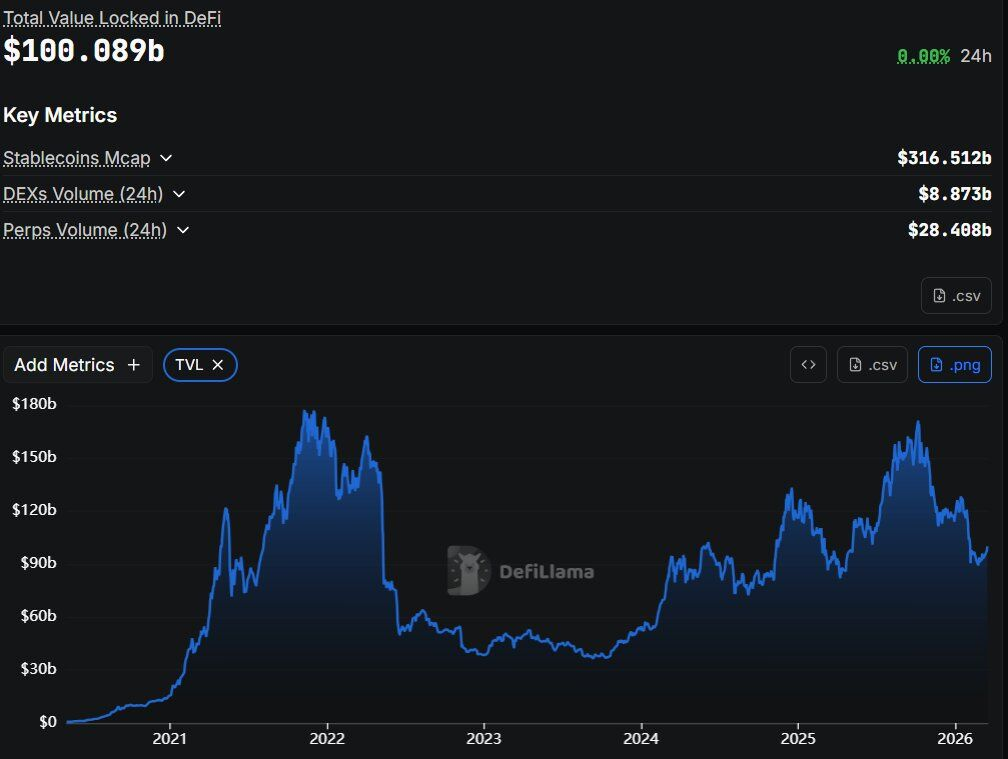

The adoption rate of DeFi technology is rapidly increasing. In just a few short years since its introduction, it has achieved over $100B in TVL, helping it draw attention from TradFi incumbents.

We are seeing traditional financial stakeholders embrace the benefits that DeFi can bring for them and their customers. However, great care is being taken to ensure privacy and reliability remain the highest priority.

You might begin seeing banks and credit card companies utilize stablecoins, which are onchain facsimiles of fiat currency. There is also agrowing contingent of financial institutions exploring tokenization of real-world assets (RWAs).

Reach out to BCW today to discover how your firm can benefit from DeFi integrations and infrastructure!